THE INCREDIBLE SHRINKING MODES. ✈️

ALAWAI’I AIRLINES?

(9/20/24)—After jettisoning the JetBlue-Spirit merger☟, the US Department of Transportation has instead approved a marriage between Alaska Air and Hawaiian Airlines, albeit with several caveats.

Closing within days, the merger agreement stipulates that established key routes (to/from, between the Sandwich Islands); frequent-flyer miles/loyalty; gratis family seating and consumer service protections (for six years, no less) are ensured by both carriers. The combined airlines will otherwise operate separately, maintaining their respective brands/colors. Together, they will become the fifth-largest US carrier, capturing some 50% of mainland-to-Hawai’i air travel traffic.

consumer service protections (for six years, no less) are ensured by both carriers. The combined airlines will otherwise operate separately, maintaining their respective brands/colors. Together, they will become the fifth-largest US carrier, capturing some 50% of mainland-to-Hawai’i air travel traffic.

This constitutes the first major US airline merger since Alaska bought Virgin America in 2016, coming at a time when Justice Department antitrust regulators have looked askance at further industry consolidation. So aloha, Alawai’i or no—we’ll see what happens to fly from here. Mahalo… (MTC…)

![]()

SOUTH BY SOUTHWREST?

(8/4/24)—Free love is under attack, and it appears to be bordering on an inside job. For poachers/plunderers have a foot in the cockpit door, aiming to double down nonstop.

Gone are the hot pants and short shorts, the luv carts, free peanuts and cheeky, winking ‘fly me tonights’: all the no- frills, no-fee fuss. Going before long could be Southwest Airline fan favorites like open seating and cozy legroom, with its free bag policy up for grabs.

Why? Because after soaring over 47 straight profitable years, SWA began hitting stormy weather during the pandemic year, 2020, and has been feathering, weathering by comparison ever since. Thus quarterly revenue projections and share prices started trending southward (down by nearly 50% over the past three years). Same time, fleet capacity has stalled due to its exclusive dependency on 737 aircraft and Boeing’s post-MAX delivery delays—especially of a key smaller MAX 7 variant yet to be certified.

So Dallas-based Southwest has zipped-up some, trimmed hiring, resorted to cutting flights and point-to-point secondary airports with weaker load factors such as Bellingham,  Washington; Syracuse, New York; GW Bush International in Houston, even Cozumel, Mexico—Atlanta and Chicago O’Hare also in the crosshairs.

Washington; Syracuse, New York; GW Bush International in Houston, even Cozumel, Mexico—Atlanta and Chicago O’Hare also in the crosshairs.

Then came SWA’s massive December, 2022 winter storm meltdown, nearly 17,000 canceled flights, passengers stranded through the holidays—for which the carrier is still paying, in record fines and compensation. Moreover, the FAA has now launched an investigation into recent ‘close calls’, wherein different Southwest flights have 1) cruised but 150-ft. over Tampa on approach and 2) come within 400-ft. of crashing into the ocean off Kauai, Hawaii.

Getting the Yoke?

None of this escaped the analytical scrutiny of Elliot Investment Management—activist hedge funders who know corporate underperformance opportunities when they screen it. Scooping up a nearly 11% ($1.9bn) position on SWA, Elliot instantly became one of its major investors, and critically hyperactive about it. This with Artisan Partners Global Value already owning some 1.8%.

hyperactive about it. This with Artisan Partners Global Value already owning some 1.8%.

So enter the trough-feeding hedgehogs, who soon called for a takedown of Southwest management and ‘feckless’ old board of directors—smacking of notorious strip-and-sell tactics already decimating the newspaper industry, et al. Citing a failing operational strategy, over-dependence on troubled Boeing aircraft and underdevelopment of (outdated) technology systemwide, Elliot further posited a post-pandemic air travel market: One that soars toward more ‘premium economy’ comfort and amenities, plus better seatback entertainment, with passengers willing to pay their way. And that SWA must get on board ASAP.

Yet Southwest CEO Bob Jordan (since 2022) maintains that he’s not going anywhere. Instead the carrier intends to adopt a ‘poison-pill’ defense if necessary to counter Elliot’s attempt to strengthen its ownership stake—much less wrest fuller control by staging a hostile takeover. A diluting ‘pill’ action entails SWA issuing trade rights to each common stock share, enabling exercising holders to purchase more shares at a discount, should any party move to take a larger than 12.5% position.

strengthen its ownership stake—much less wrest fuller control by staging a hostile takeover. A diluting ‘pill’ action entails SWA issuing trade rights to each common stock share, enabling exercising holders to purchase more shares at a discount, should any party move to take a larger than 12.5% position.

In turn, Elliot intends on waging a proxy battle to oust Southwest’s 15-person board via ‘padded share’ voting. The hedge firm has set a September 9 showdown meeting with proxied shareholders so as to give them a direct say on who should run the airline going forward.

Fraying the Course?

Nevertheless, the carrier has since signaled that some of the Elliot activists’ advisories are in play. Hence SWA’s rather recent announcement that its hallowed open-seating policy may eventually take a back one to premium assigned seating plans and roomier seat rows as a means of boosting revenue (by upwards of $3.4bn per annum, say analysts), with bag fees hanging in the balance. Such changes will be subject to regulatory green lights and require reconfiguring its airplanes however—while the Elliot gang considers them too little, too late anyway.

In any event, many Southwest’s employees fear activist pressure poses an outside threat to the carrier’s fabled Herb Kellehaha ‘Coheart’ culture. They note that the airline already sells Earlybird Check In and Upgraded Boarding as it is, with a similar assigned-seating gambit proving too cumbersome in 2006.

proving too cumbersome in 2006.

Southwest customers may bag to differ on all this as well, remaining faithful to the carrier’s ‘egalitarian’ open seating, however chaotic and contentious its boarding scenes can be. These loyal fans still prefer its simpler booking process, and contend that not everyone wants nor needs pricey frills when they fly. More to the point, Southwest claims nearly 50% of its business owes to that very first-two-checked bags-free policy. So bottom line: assigned seating maybe, but bag fees be damned.

Now whether SWA takes on this culture war, wrestling with its activist investors over freedom versus feedom—or whether spirited customer loyalists form SWAt teams to take out the sharpie hedgehogs altogether—time and temerity will likely tell. UPDATE: Southwest has since agreed to board member changes Elliot ‘recommended’—involving the appointment of four new directors, likely three of whom will come from the EIM slate. Moreover, whether present CEO Bob Jordan survives this purge remains to be seen. Vamigré can only hope no more love is lost in the fray. (MTC…)![]()

FARE BONANZA or UNFAIR BOTTOM FEEDING?

(2/24/24)—Recent reports that three different jetliners topped 800 mph (American Air and Virgin Atlantic upwards of 840 mph), noted as how the trans-Atlantic flights to London had caught momentous, earth-spinning tailwinds.

Similarly, Big Four US airlines are riding post-pandemic tailwinds these days, and are feeling mighty hale and grabby about it. But the same cannot be said for comparatively smaller, low-cost carriers that are instead facing equally powerful headwinds not entirely of their own mapping.

and grabby about it. But the same cannot be said for comparatively smaller, low-cost carriers that are instead facing equally powerful headwinds not entirely of their own mapping.

Heads or Tails?

The majors’ route to current air superiority uses hub, fleet, booking, amenities and miles/loyalty to their bottom line advantage—namely key operational and fiscal resources to better ride the tailwinds, weather any storms. Budget carriers not so much, having as they are to compete primarily on price, headwinds ever on the nose and flight deck altimeter.

Fuel, labor, staffing, fleet greening and new plane delivery delays: who better equipped to navigate today’s challenges and turbulence as the surging demand for air travel begins returning to the pre-pandemic mean? Little wonder we’re already hightailing it the legacies’ way for that ‘fare bonanza’ in early 2024, enabling the major carriers to fly and ply less friendly, more predatory skies.

For with their everyday business travel being reined in (via Zoom, remote work and the rest of it), the Bigs are currently vectoring their coordinates toward the leisure sector. Further, anticipating that 2023’s surge of international travel may be leveling off, they appear to be zeroing back in on domestic US routes—and the bargain carriers that have been feeding (and feeding off ) them for decades now, even as they have been nibbling at the Big’s major hubs with fare-war discounting themselves. Fair enough—when the legacies  were milking steady full-service business class traffic, they were content to leave us economy class hoi polloi at the discounters’ teeming gates.

were milking steady full-service business class traffic, they were content to leave us economy class hoi polloi at the discounters’ teeming gates.

But with soaring fuel and labor costs, strikes and shortages ever looming, the Big Four are taking aim at the low- and ultra low-cost airlines’ no-frills flight plans: namely jettisoning advanced seat assignments, adding checked bag fees, tightening change/refund restrictions, trimming seats and overhead bins to lure ‘priced-out’ air travelers. Only the mainline carriers bring their own ‘bare-bones’ basic economy fares to the counter and screen, overshadowing the discounters price-wise, while adding bennies like scheduling frequency, flight reliability, robust miles/loyalty programs, and onboard service/amenities to lure many post-pandemic/revenge travelers who welcome a skosh more concourse-to-cabin comforts by now.

Addition by Attrition?

So L-Cs and UL-CCs alike suddenly find themselves losing their pricing power with major carriers gearing to pick them off. Facing the same operating costs and staffing shortages, the budgets can do little but continue to slash fares to fill their sardine seat rows, as their share values and market cap valuations nosedive. Hampered by horror stories of à la carte fee-for-alls, mobbed ticket counters and kiosks, rampant flight delays/cancellations, slim seating and mishandled baggage, some may cut capacity, tighten or trim their courses and tread air for brighter skies, or peel away altogether.

Beyond JetBlue’s desperate, failed attempt to absorb Spirit Airlines☟, the latter lost almost $160m in Q3 2023 and threatens Chapter 11, as rival Frontier Airlines lost $32m. Even Big #4 Southwest Air, which was still paying for its 2022 holiday meltdown, suffered a per seat/mile unit revenue swoon of nearly 11% toward year’s end. Thus bargain carriers are paring routes and flight frequency—Frontier offering “All You Can Fly” winter passes for $299—as the ‘bottom feeding’ big-boy airlines take territorial aim. On that score, major Euro discounters like Ryanair and EasyJet currently find their profits in downdraft as well.

Spirit In The Skies?

(Update: 4/10/24)—As for Spirit Airlines, the carrier appears to be a somewhat dispirited outfit right about now.

Its JetBlue marriage plans having been annulled by the US Justice Department and Massachusetts Federal Court as anti-competitive and traveler unfriendly, the ultra low-cost has announced a stall maneuver on delivery of new Airbus planes for 2025 through 2026.☟ Accordingly, the Miramar, Florida-based airline will in turn adjust to the fleet trim, furloughing some 260 pilots by September 1, while seeking mitigating voluntary crew reductions from pilots and flight attendants alike.

All this comes in an effort to ease current financial pressures and increase liquidity by $340m in the next two years. Spirit executes these moves as it posts operating losses in six straight quarters, despite non-stop  surging travel demand. The ULC carrier considers cutting flights, even abandoning some markets to boost profitability further—citing fare-per-passenger levels down 25% in Q4 2023 alone, blaming heavy discounting amid excess capacity overall, which allays pricing power/leverage.

surging travel demand. The ULC carrier considers cutting flights, even abandoning some markets to boost profitability further—citing fare-per-passenger levels down 25% in Q4 2023 alone, blaming heavy discounting amid excess capacity overall, which allays pricing power/leverage.

Striking Accords.

Spirit says it has reached agreement with Airbus SE that 2025-26 aircraft deliveries will be deferred to 2030-31; scheduled 2027 through 2029 orders remain unchanged. This will leave the carrier’s all-Airbus fleet at 219 planes in 2025, down from a previous target of 234—capacity pared by 7% in 2025, 16% in 2026.

Moreover Spirit has finalized a compensatory agreement with supplier Pratt & Whitney (worth $150m-$200m) over another ongoing issue: the quality and reliability of P&W’s Geared Turbofan (GTF) engines—to where an average of 40 of the carrier’s A320neo jetliners are thus sidelined monthly.

Now whether such financial refueling can silence analyst calls for the struggling airline’s bankruptcy/ liquidation remains up in the air. At any rate, safe to say that the carrier’s most recent flight plan to add California routes (e.g., SF>SD) signals that its fiscal straits and storms will not ground this Spirit in the sky anytime soon. (MTC…)

Making the Call.

But wait—despite facing similar headwinds, other low-fare carries are faring comparatively well in recent airline surveys. Ratings of 2023 airline performance found five of the top carriers coming from the budget/low-cost tier—bettering on-time performance, lowering flight cancellations/delays (‘CanDels’), cutting down bump and dumps, easing baggage mayhem and miscues.

bump and dumps, easing baggage mayhem and miscues.

Alaska and Allegiant Airlines ranked particularly high. Allegiant, a streamlined Las Vegas-based discounter flies non-stop routes with a smaller market strategy of avoiding layovers and upfronting its fees—from seat assignments to checked and carry-on bags. Besides, Houston-based bargaineer, Avelo Air is expanding routes throughout the western US, while Canadian upstart Lynx Air is launching ‘ultra-affordable’ round-trip service from Toronto to East Coast cities and San Francisco this May.

Point being, low-cost carriers are not likely to be giving total ground or sky to the ‘bottom-feeding’ poachers any time soon. Especially since American and United Airlines are flexing their wings and signaling the Big squeeze is already on by boosting bag fees to $40 per piece. Indicating this may be but a momentary fare fall en route to sky higher fee/fares come spring.

So we may want to pause before coin tossing true bargain fare carriers under the jetway for some major coin flipping, flinging around—regretting it when LC/ULC alternatives and their competitive pricing pressure are financially grounded or gone.

For when it comes to air travel, Vamigré is decidedly pro-choice. Indeed, more the better is more our speed, best outcome being heads we win, tails we win either way. (MTC…)

![]()

MERGER PURGER.

(1/30/24 +)—As to the largest airline marriage in over a decade, Spirit was willing but the case was weak… (Update 3/3/24): Accordingly, the JetBlue-Spirit merger deal has since been officially jettisoned, with JB required to Pay Spirit a $69m breakup fee, no less. Now whether this saga is in fact a ‘victory for travelers’, and has any bearing on the proposed Alaska Airlines-Hawaiian Air merger, remain to be seen. ☟

…So determined federal Judge William G. Young of the US District Court for the District of Massachusetts, who recently torpedoed the proposed merger between JetBlue and Spirit Airlines. His ruling was immediately declared an anti-consolidation victory by the Justice Department and big win for cost-conscious travelers.

To refresh see☟, Judge Young’s decision constitutes rather climactic blockage to a merger effort that has been up in the air for some two years now. JetBlue has courted Spirit in a post-Pandemic environment that finds large airlines rebounding more competitively stronger, while lower-cost carriers lag by comparison. The ‘upstart’ New York-based airline that claims to be a “disrupter nationwide” sought to join forces first via a Northeast partnership with American Airlines (itself shot down by Justice on anti-concentration grounds), then pivoted to acquiring ailing Florida-based Spirit Air—long battling with Frontier Airlines for the opportunity, eventually outbidding the Denver-based budget rival with a straight cash offer in 2022, swiftly signing a merger agreement with Spirit Air.

JetBlue contends that the planned ($3.8bn) marriage would make it the fifth largest US airline with some 10% of domestic market share, far better able to compete with the Big Four. JB cites its record of exerting downward fare pressure in markets it’s already entered—vowing to divest conflicting airport gates and minimize route overlap. For its part, struggling ultra low-cost (ULC) carrier Spirit maintains it is all in on the alliance.

Chapter and Reverse?

However, federal antitrust enforcers countered that the merger would only enable JetBlue to become just as market dominating as majors like United, American, Delta and Southwest—arguing that the larger carriers grow, the worse things go. For one thing, Justice pointed to the culture clash between JetBlue’s cushier, roomier comfort and Spirit’s sardine cramped but greater capacity cabins—and that JB has already signaled it would remove a number of Spirit’s seat rows posthaste.

Judge Young appeared to agree, concluding that the traveling public is better served with two stand-alone carriers here, essentially leaving JetBlue and Spirit swooping at the altar. He reasoned that an independent Spirit Airlines is important as a lower-cost alternative to hub dominating legacy carriers in terms of keeping service up and fares down.

Both carriers are appealing Judge Young’s verdict; each continuing to lose money into 2024. JetBlue, with stock shares lately sinking nearly 5%, warns that it may drop its attempted Spirit takeover altogether. Spirit, share price having plummeted over 47% since the news, faces a $1.1bn debt maturity coming due in  2025, and is being further revenue slammed by larger predatory carriers undercutting its fares. Costs rising, cash burning, the low-cost line hints at Chapter 7 liquidation, if not Chapter 11 bankruptcy to reset its financial plight. Same time, it does make note of the whopping breakup fee JetBlue agreed to in 2022, should federal regulators somehow block the merger. Red, not white flag waving JetBlue’s way?

2025, and is being further revenue slammed by larger predatory carriers undercutting its fares. Costs rising, cash burning, the low-cost line hints at Chapter 7 liquidation, if not Chapter 11 bankruptcy to reset its financial plight. Same time, it does make note of the whopping breakup fee JetBlue agreed to in 2022, should federal regulators somehow block the merger. Red, not white flag waving JetBlue’s way?

The judge and Justice Department surely intended to preserve Spirit’s independence, but it remains to be seen whether market forces will buy in. On tenterhooks as well are Alaska and Hawaiian Airlines, which seek a merger to solidify West Coast service—leing low, hoping Justice will extend a bit more aloha spirit there. For such budget carriers have not been faring well of late, what with more rigorous regulatory scrutiny, fuel and labor costs rising, new aircraft deliveries slowing, contaminated engine parts cropping up on planes they do have. In all, the makings of a steeping merger stew…

Incidentally, that big carrier low-ball poaching extends to the EU, where Lufthansa Airlines’ purchase of a minority stake (41%) in ATA Airways (formerly Alitalia) is under European Commission investigation on anti-competitive grounds—Wizz Air and Ryanair growth or no.

At any rate, we flighty travelers may not know what we’ve got until we lose it, and the legacies tighten the airfare screws again. (MTC…). ☟![]()

SHRINK WRAP: 2023.

Banking toward matters of airline capacity, we see it doesn’t take a board certified shrink to diagnose notable changes in travel patterns and directions these post-pandemic days.

People work more flexibly, smartphone it in remotely, legions of retiring VamoSilvers are growing and going all the more. So while travel remains robust into the peak spring/summer season, the hidebound ‘when and where’ clotting and cattle calls are finally beginning to volplane. Increasingly tech-fed travel consumers are booking trips earlier and more strategically often. And with carrier change fees easing, we are making last-minute (‘plan B’) bypasses/redirections more frequently.

Airlines are certainly taking note, adjusting flight capacity accordingly. Case in point: current TSA stats do indicate a 14% drop in Tuesday and Wednesday traffic, but steadily stronger rebounds Thursday through Monday. So carriers such as Delta and Frontier are reportedly cutting flights by some 20% midweek, then hiking fares for peak-day flights—calibrating, if not throttling capacity, then overstuffing scheduled planes. This, while certain low-costers ‘ghost’ (scrap) their flights by the hour and day, leaving passengers in terminal no-go limbo.

through Monday. So carriers such as Delta and Frontier are reportedly cutting flights by some 20% midweek, then hiking fares for peak-day flights—calibrating, if not throttling capacity, then overstuffing scheduled planes. This, while certain low-costers ‘ghost’ (scrap) their flights by the hour and day, leaving passengers in terminal no-go limbo.

In all, airlines call it adjusting to a ‘new normal’ of further-out booking, close-in switching. They claim that these emerging pattern shifts threaten to further dent their load-factor and revenue projections, at a time when crew strikes, fuel spikes and ground labor shortages pose stiffening headwinds. Not to mention Biden Administration pro-consumer jawboning, and the judicial quashing of the JetBlue-Spirit merger and JB’s Northeast Alliance arrangement with American Air: Both verdicts on the forceful Department of Justice actions are pending appeal.☟

Nevertheless, Vamigré once again sees airlines rather shrinking fleets to fit their bottom lines, fixin’ to cause beset travelers more fits. So track, we will. But that’s the latest shrink rap/wrap, for starters…

![]()

☟ HAWAIIAN AIR RAID?

(12/7/23)—With winter months scrolling onto its touch screens, Alaska Airlines has announced that it is warming up to Hawaiian Airlines in an ardently acquisitive way.

The Seattle-based carrier seeks to purchase the Sandwich Islands’ principal airline for $1.9bn from Hawaiian Holdings, Inc., stressing that the merged airlines would continue flying their separate brands and colors as they combine to increase their slice of Hawaii’s some $8bn annual passenger revenue pie –also expanding routes to Asian markets beyond.

Alaska’s CEO, Ben Minicucci contends that the consolidating airlines, long rivals, would become the lead dogs and dolphins to Hawaii, what with relatively little overlap (3%) in their respective route maps from major West Coast cities, and compatible aircraft fleets numbering 365 planes. The ‘great fit’ merger would allegedly better serve consumers with more flights to more Pacific destinations. And travelers would not be losing a budget airline in the process—which would take many months to implement at best.

Further, the “step change” purchase would enable Alaska Air to solidify its position as the nation’s fifth-largest carrier, and more effectively challenge the dominance of American, Delta, United and Southwest Airlines—which currently control nearly 80% of the domestic market.

As for Hawaiian Airlines itself, the carrier apparently welcomes Alaska’s lifebuoy, however lukewarmly. Because the Islands have faced a stream of challenges post-COVID: Namely slow visitor/revenue recovery, growing competition from SWA, aircraft delivery delays, and Maui’s wildfire devastation—to where Hawaiian Air has suffered net losses over 14 of the past 15 fiscal quarters.

Also factoring in is the reality that domestic (‘revenge’) travelers have been ranging increasingly international these days—another reason why Alaska’s Minicucci sees the deal offering a “tremendous  amount of upside” all around.

amount of upside” all around.

Upside Downsides.

Still, there is something of a chill in the air over this entire palmy arrangement—and how it actually threatens to reduce price/service competition in the mainland-to-Hawaii sector by boosting combined market share to nearly 40%, double that of the next entrant, UAL.

This, while the federal Department of Justice continues to look askance at such airline industry consolidation (e.g., majors gobbling up smaller players’ planes and gates/slots), already filing suit to block JetBlue’s own ‘existential’ takeover of low-cost carrier, Spirit Air for $3.8bn—just after scuttling JB’s East Cost partnership with American Airlines. A federal judge in Boston is expected to rule on that Spirit acquisition in coming days, with vigorous industry competition and price-conscious traveler concerns holding in the balance. ☟

At any rate, it can be argued that the larger an airline becomes, the higher its fares/fees rise, the more flight selection/service decreases and seats/storage shrink in kind—revenue/profit margins never deemed profitable enough. Then there is the less-is-more specter of anti-competitive and consumer ‘harming’ hub/route monopolies, not to mention potential price-fixing collusion with impunity.

It appears only the federal courts, Justice Department (+ FTC) stand in the way of further airline consolidation—Anti-Merger Act of 1950, pandemic bailout leverage, union demands notwithstanding. So we may see a clearer touch screen on the JetBlue-Spirit case by mid December at the latest.

For their part, Hawaiian Holdings investors will likely be voting on the merger deal early in 2024. Meantime, Alaska Airlines basks in the glowing prospect of greater Island access and bountiful aloha spirit, even though Hawaiian air-raid sirens may instead be blaring in early-warning mode. (MTC…)

![]()

☟PLAYING SOME SPIRITED JETBLUEs.

(10/31/23)—The US Justice Department has now pressed a federal judge in Boston to block the pending JetBlue-Spirit Airlines marriage, after filing an antitrust suit to throw wet rice on the entire $3.8bn affair—determining it to be ‘against the public interest’. Attorney General Merrick Garland had concluded that a merger of two ‘budget’/ULC rivals would result in reduced competition and increased prices, putting “… travel out of reach for many cost-conscious travelers”: Namely via a 30% fare increase on the combined routes, according to JetBlue’s own projections, costing passengers upwards of $1bn in harm per annum.

Scarcely helping the carriers’ case is that JetBlue’s aggressive, if not hostile attempt at creating the fifth largest US airline by 2024 (wishful thinking?), had already rankled federal regulators by forging a cozy  Northeast Alliance with American Airlines to more easily reserve/sell one another’s seats. Add in rumors that any newly merged JetBlue flights would offer fewer economy class seats (wow, that’s the Spirit!).

Northeast Alliance with American Airlines to more easily reserve/sell one another’s seats. Add in rumors that any newly merged JetBlue flights would offer fewer economy class seats (wow, that’s the Spirit!).

(Update 5/20/23)—A federal judge has since struck down that Northeast Alliance as a non-competitive ‘back-door’ merger in the making—a consolidating, cross-feeding partnership of heretofore fierce rivals that would stifle East Coast competition and raise fares, potentially costing travelers hundreds of millions of dollars per year.

The proposed major airline merger itself, which would have been the first in the US since Alaska’s takeover of Virgin America in 2016, aimed at landing 10% of the domestic commercial market. JetBlue holds that it is truly a ‘bargain’ brand, lowering fares in whatever market it has entered, to more or less ‘disrupt’ the legacy carriers.

But DOJ countered that Spirit is really an ‘ultra low-cost’ (ULC) airline, (albeit via higher fees), that frequently takes on the majors in their own markets nationwide. That JetBlue hews more toward Big Four domination, and the merger would seriously dull Spirit’s feisty competitive edge—not least along the East Coast, connecting down to the Caribbean.

New York, Massachusetts and District of Columbia have joined the Justice Department suit, as since have Connecticut, New Jersey, Maryland, North Carolina and California. So absent any negotiated resolution, brace to see them in court, and over the long haul, to be sure. (MTC…)

(10/20/22)–The final draw: All along, Spirit Airlines essentially played fellow discounter Frontier Group Holdings Inc. as a hole card to keep an already ‘blue-chipped’ JetBlue anteing up—no matter how the principals now spin it.

✈️ After months of bitter public haggling, four voting delays, Spirit investors trumped the carrier’s own board and handed its craven yellow jets over to JetBlue for a pot-busting $3.8bn cash. Once Frontier folded—standing pat and refusing to overbid beyond its $2.9bn cash-and-stock offer—JetBlue swooped back in, heaping planeloads of greenbacks on disSpirited stockholders to seal the deal.

The new, ostensibly conjoined carriers say their marriage, now fully shareholder approved, will be consummated by the second half of 2024, launching operations as the fifth-largest US airline (w/10% of the market) early in 2025. But that flight plan hangs on Justice Department regulatory approval of the merger, which is no pat hand given DOJ’s vigorous opposition to a current JetBlue-American Air Northeast Alliance (NEA) partnership, amid Biden administration antitrust concerns.

If, as Frontier has predicted, regulators nix the JetBlue-Spirit sale as being anti-competitive in an already over-concentrated airline industry, JetBlue will still owe Florida-based Spirit $70m and its shareholders a $400m ‘reverse breakup fee’. Either way, JetBlue will also be paying Spirit a monthly 10¢ per share ‘ticking fee’ from January 2023 until the deal fully closes.

Winner’s Losing Hand?

JetBlue’s blue-sky projections aside, the New York-based airline faces a long uphill slog to regulatory rice and bouquets. Industry analysts view its Spirited splurge a desperate move by an antsy higher-end budget carrier in dire need of precious pilots and more Airbus A320 aircraft—one now entering into  years of swampy cross-cultural integration with a spotty banana yellow discounter like Spirit.

years of swampy cross-cultural integration with a spotty banana yellow discounter like Spirit.

For its part, jilted Frontier is perhaps better suited for a powerful lone-ranger role as lead cowpoke in rapidly growing ultra-low-cost carrier territory, with a “lot of runway ahead.” And fuller saddlebags at that, since it will receive $25m from Spirit for its merger-related troubles, and $69m more upon Spirit’s striking the deal with JetBlue or any other carrier over the next 12 months, for that matter.

In any case, those same analysts note that passengers are usually losers in such consolidation plays; moreover “…we have yet to see an airline merger in the US over the past 30 years that has been good for consumers, labor…or even for the cities and regions in which they operate.” We will see about that…

Otherwise, both Spirit and JetBlue, lowly 6th and 10th respectively in recent D.O.T. on-time performance ratings, have announced they would continue to operate independently with customer loyalty ledgers unchanged until this high-flying merger is officially cleared to land.

Until then, we’ll hold tight, flush with questions, seeing a bluffer’s bet that may well crap out before it actually wheels down onto the tarmac. (MTC…)

(7/15/22)—At a time when Spirit Airlines suffers a fiery landing gear touchdown in Atlanta, this was not the only iffy/heated landing the Florida-based ultra lowfare carrier is executing these days.

✈️ The latest development: Four of a kind beats a wait? Nominal bidding frontrunner Frontier Group Holdings Inc. has requested a pause (to July 15) in Spirit Airlines shareholders’ vote (yet again) to give Frontier more time to sell its “last, best and final” proposal to more skeptical investors. Spirit’s board has obliged, extending the vote deadline until July 27, publicly continuing to prefer the Frontier scenario. It is essentially the fourth delay in this months-long merger saga, which finds rival JetBlue relentlessly sweetening it ante (now up to $3.7bn cash plus a per-month prepayment dividend), gradually wearing down the pro-Frontier Spirit boardroom crowd by the day.

Frontier holds fast to its bid ($2.7bn cash/stock), with a wild card of reverse termination fees should the US Justice Department ultimately nix the merger on grounds of anti-competition. Cushier low-cost niche player JetBlue has upped its firm breakup fee to $400m, while Denver-based Frontier counters with a $350m fee. New York-based JetBlue maintains that its wing-and-prayer proposal offers a better chance of federal regulator approval, despite a DOJ suit to block JB’s partnering with American Airlines. Moreover, proxy-advisory firm International Shareholders Services (ISS) advises the Spirit board to accept the “clearly superior” JetBlue offer its has been rejecting for months now in favor of Frontier’s truer budget-to-budget carrier marriage and its likelier prospect of passing regulator scrutiny.

The Frontier CEO doesn’t exactly exude mountain man confidence by now, his carrier remaining “very far” from corralling enough Spirit shareholder voters to seal the deal. Yet committed Frontier stays (that’s the Spirit!), whereas JetBlue is “…ready to enter a binding agreement with Spirit as soon as practicable…immediately following Spirit shareholders voting against the Frontier (bid) on July 27.”

Pot’s Right?

The increasingly bitter bidding gamble has been poison to both JetBlue’s and Frontier’s stock prices, but the Spirit jackpot—and it unifying promise of instant 5th largest Big Air carrier status—appears to be a payoff too ski high to pass up or eventually fail. So, very public negotiations and advertising campaigns aside, two questions obtain after all these months:

Is JetBlue’s aggressive obsession with ultra lowfare Spirit Airlines coming out of strategic vision/ strength or fiscal, existential desperation? Conversely, will Frontier’s quieter, stand-pat strategy prove to be its last merger rodeo?

We travel consumers will soon discover whether a New York takeover artist or Colorado cowboy justice will at long last win this Spirited aerial showdown, and what it will mean to us. Nevertheless it is looking to be a bumpy, if not fiery landing either way. (MTC…)

(6/2/22)—Now look at what the Jet Stream Blue in: a $3.6bn counter offer for Spirit Airlines in a bid to expand its fleet and fly with the Big Four (namely American, United, Delta, Southwest= 66%+ of market).

✈️ Make that an all-cash lure (continuing to be rejected by Spirit Airlines, which cited thoroughly ‘unacceptable’ regulatory risk—leaning back toward Frontier’s offer as a better low-fare fit. JetBlue differs, so let another shareholder vs. seatholder battle begin):

Next step, JetBlue launches a hostile takeover ’tender offer’ directly to Spirit shareholders at $30 per share, $3.2bn total…nevertheless, Spirit’s board continues to urge rejection of JetBlue’s “risky…cynical” bid. But JetBlue keeps sweetening the pot, offering a higher ($3.4bn) deal, with an (anti-trust) breakup fee of $350m, prepaid as a shareholder dividend. Frontier stands pat (incl. a $250 breakup fee), and Spirit’s board members suggest they will play their hand later this month. Again, JetBlue’s aggressive bidding is meant to occlude the Frontier-Spirit merger plan announced in February☟—which was seen as forging a rival ultra-low-fare (U.L.C.C.) giant with compatible fleets of Pratt & Whitney-powered Airbus A320s. Affording cheap fares, albeit with minimal service and fees for select seating, checked bags and most everything else, that combined airline would supposedly comprise 10% of the domestic market and save passengers $1bn per year.

However JetBlue cites its “superior proposal”: a larger, more powerful challenge to the Bigs, grabbing some 8% of the US market while also bringing fares down. Such a “perfect match” with budget carrier Spirit would boost its fleet to 450 mainly Airbus planes—by retrofitting some Spirit aircraft—with 300+ more ordered over the next six years.

Primarily a domestic US carrier, New York-based JetBlue could gain system range, given Florida-Based  Spirit’s routes along the East Coast, legacy hubs west (Memphis to Dallas) and across the Caribbean and Latin America. This marriage would presumably establish a formidable ‘Fifth Major’ in market share (adding in JetBlue’s current coordinating ‘de facto merger’ arrangement with American Airlines), ostensibly offering low fares and “a greater travel experience.”

Spirit’s routes along the East Coast, legacy hubs west (Memphis to Dallas) and across the Caribbean and Latin America. This marriage would presumably establish a formidable ‘Fifth Major’ in market share (adding in JetBlue’s current coordinating ‘de facto merger’ arrangement with American Airlines), ostensibly offering low fares and “a greater travel experience.”

Not Surprisingly, Frontier (and its $2.9bn offer) argues that it and Spirit share more complementary bargain-fare, point-to-point business models in distinctly different regions. The Denver-based carrier paints JetBlue’s bid as creating East Coast overlap that would actually decrease competition, resulting in “more expensive travel”, since JetBlue is a decidedly higher-fare carrier known for its lie-flat beds seating, free Wi-Fi and full-serve meals, at least in premium business class.

Spirit itself has simply said the “unsolicited” JetBlue offer would be evaluated “…in the best interests of Spirit and its stockholders” within 10 business days—with of course little or no regard for us travelers. It also must be said that JetBlue is playing all sorts of hardball cards, not least filing ‘Vote No’ proxy statements to Spirit shareholders to reject the Frontier offer, while slinging mud at Frontier’s controlling management and Spirit’s board member ties with private equity outfit, Indigo Partners.

As to all that, Wall Street and most airline industry analysts quickly red-flagged the confounding, ‘out-of-the-Blue’ bid—skeptical that either merger would actually deliver as promised—none of the three carriers playing a particularly strong hand. For a time, JetBlue and Frontier shares were down some 8%, Spirit itself down over 3% before bouncing back. Clearly, these consolidation plays come amid a post-pandemic scramble for pilots, flight attendants and staffers as travel demand rapidly rebounds.

But whether the Department of Justice antitrust regulators climb aboard is another matter, since the Biden administration has already nixed the proposal for a more formal “Northeast Alliance” between American Airlines and…JetBlue.

Seems like more than ATC snags and congestion are affecting the overcrowded Florida skies these days. So will it be ‘pass the Spirits’, ‘thar she Blues’, or a rather expansive new Frontier? We still shall see…(MTC…)

☟CROSSING A DiSPIRITING FRONTIER?

(2/8/22)—If it’s not a flight, it’s a fleet. If it’s not a scheduling purge, it’s a carrier merge: Yet do two negatives make a positive?

Frontier and Spirit say positively, roger that, as the super low-cost airlines announce their plans to join forces, doubling down in a $6.6bn deal, essentially creating the nation’s fifth largest US carrier overnight. They would thereby be offering 1,000 daily flights to some 150 destinations in the US, Caribbean and Latin America. Even though their merger fanfare did face a rather inauspicious takeoff, with 130+ of Frontier’s flights and 25% of its operations being same-day grounded by a system-wide technical breakdown (said to be ‘quickly fixed’).

Nevertheless, Colorado-based Frontier is set to become the purchasing partner (51.5%), buying Spirit for $2.9bn in cash and  stock. It brings its Western states network to the marriage, while Florida-based Spirit provides broader Eastern US coverage and more international routes. Both carriers fly only Airbus A320 series jetliners, fleets expecting to grow from 280 (combined) to upwards of 500 by 2026.

stock. It brings its Western states network to the marriage, while Florida-based Spirit provides broader Eastern US coverage and more international routes. Both carriers fly only Airbus A320 series jetliners, fleets expecting to grow from 280 (combined) to upwards of 500 by 2026.

Targeted for a second-half 2022 close, this proposed fusion would vault ‘Frontier/Spirit’ past JetBlue and Alaska Air in terms of total miles flown by paying passengers, forging a giant budget carrier bested domestically only by the four biggies: American, Delta, Southwest and United—which control some 80% of the total airline market. It comes at a time when the three low-fare carriers (+ Allegiant) are rebounding more robustly from the pandemic downdraft (Q1 travel capacity per seat miles up 21-29% from 2019) than those lagging majors (down 16-18%). Because the leisure sector is surpassing business travel in passenger traffic lately—crammed coach seats faring better demand-wise than cushier first-class digs. Reason enough why their growth plans are soaring sky high.

No denying both airlines have suffered losses in the past two years. Spirit posted a $440.6m deficit in 2021 (federal assistance or no), after a far redder 2020 of $719.6m. Frontier lost  $299m in 2020 and 2021. Still, their respective CEOs claim their merger will yield an aggressive ultra low-fare competitor to the majors with more consumer-friendly fares, thereby “saving passengers some $1bn per year”) and affording better point-to-point service (e.g., to underserved smaller cities) in this booming leisure travel market. They say a combined Frontier/Spirit will also create 10,000 new jobs by 2026, with destinations and communities also benefitting—i.e., win, win all around.

$299m in 2020 and 2021. Still, their respective CEOs claim their merger will yield an aggressive ultra low-fare competitor to the majors with more consumer-friendly fares, thereby “saving passengers some $1bn per year”) and affording better point-to-point service (e.g., to underserved smaller cities) in this booming leisure travel market. They say a combined Frontier/Spirit will also create 10,000 new jobs by 2026, with destinations and communities also benefitting—i.e., win, win all around.

Then again, the two no-frills airlines bring dismal customer satisfaction ratings to the bargaining jetway. While both offer dirt-cheap base fares and minimal service, they routinely tack on extra fees for most everything else, not least carry-on bags. Spirit, which basically invented ‘ancillary revenue streams’, amassed the highest number of complaints (13.25 per 100,000 passengers) in Q1-3 2021, while Frontier rated 5.56 per, after a bruising 60.24 in 2020.

Little wonder merger critics fear a truer reality of this low-fare giant devouring smaller no-frills competitors—of fewer flights to fewer cities, with negligible service at higher fares and costs, particularly as passenger traffic increases come spring and summer.

Frontier Justice?

Ultimately the plan must first cross paths with a Biden administration that is prioritizing more competition in the airline industry. It notes this is the first such merger since Alaska Air swallowed up Virgin America in 2016, and such industry consolidation has resulted in the four major carriers shrinking from ten in the past 25 years. Which is perhaps why the feds aggressively blocked a recent American Air/JetBlue domestic ‘alliance’, and antitrust regulators will likely scrutinize the Frontier/Spirit merger plan all the more. This, despite the carriers’ assertion that a service overlap in merely 18% of their total routes limits the potential reduction of competition for passengers. And the combined airlines, currently ranked eighth/seventh respectively, will still only amount to 10% of the market overall.

At any rate, the Departments of Justice and Transportation will be the judges of that, as will the carriers’ respective pilot and flight attendant unions. And Vamigré will be crossing this new Frontier as well—if and when we should actually come to it. (MTC…)

![]()

SHRINK TO FITS.

(7/15/22)—Like cheap uni khakis on high spin dry, the shrinkage continues unabated, just as travel demand surges to fitful 2019 levels and beyond.

Most recently, and internationally: British Airways cut some 10,300 flights from its summer ’22  schedule due to capacity limitations: namely pilot and staffing (particularly tarmac/ramp workers) shortages. KLM Royal Dutch trims 2,000 scheduled flights, restricting ticket sales to acutely bottlenecked European destinations—Deutsche Lufthansa (2k cuts across the Continent), Air France and easyJet PLC following suit, with little public notice. Moreover, a pilots strike (1,000+) has so crippled debt ridden SAS AB that the leading Scandinavian carrier filed for Chapter 11 protection, under more favorable US conditions, for nine months to a year, cutting 50% of its scheduled flights per day.

schedule due to capacity limitations: namely pilot and staffing (particularly tarmac/ramp workers) shortages. KLM Royal Dutch trims 2,000 scheduled flights, restricting ticket sales to acutely bottlenecked European destinations—Deutsche Lufthansa (2k cuts across the Continent), Air France and easyJet PLC following suit, with little public notice. Moreover, a pilots strike (1,000+) has so crippled debt ridden SAS AB that the leading Scandinavian carrier filed for Chapter 11 protection, under more favorable US conditions, for nine months to a year, cutting 50% of its scheduled flights per day.

Seems at a time when inflation is hammering the euro, now on a 1:1 par with the US Dollar, travelers are attracted to relatively less expensive Continental destinations, even as historic heat and wildfires now rage across Europe. Yet more Euro flagships are unfurling by the day…to where London’s Heathrow airport is asking airlines to cap ticket sales (at 100k passengers per day) for the summer into September.

Seems at a time when inflation is hammering the euro, now on a 1:1 par with the US Dollar, travelers are attracted to relatively less expensive Continental destinations, even as historic heat and wildfires now rage across Europe. Yet more Euro flagships are unfurling by the day…to where London’s Heathrow airport is asking airlines to cap ticket sales (at 100k passengers per day) for the summer into September.

This despite stern rejections from carriers such as Emirates, which charges the airport management with incompetence (as in baggage backlogs—a colossal bag lag perhaps triggered by a June conveyor belt failure), underfunding and overall consumer disregard. While Amsterdam’s busy Schiphol Airport is little better off, having set its passenger limits on June 16. (MTC…)![]()

BAKED ALASKA?

(6/8/22)—The first conspicuous stress cracks in air travel’s projected 2022 rebound are currently cleaving Alaska Airlines.

For the Seattle-based carrier continues to be hit, and hit hard, by a searing pilot ‘work stoppage’ that has resulted in well over 550 flight delays/cancellations since May 1 and counting, waylaying tens of thousands of passengers, with no contract  resolution on the horizon.

resolution on the horizon.

Over 3,100 Alaska Air pilots have forsaken their cockpits, some walking picket lines at Sea-Tac and other airports amid a nationwide commercial pilot shortage. The Airline Pilots Association union members have been locked in bitter contract negotiations with Alaska for three years, over issues of pay, job security and schedule stability. ALPA contends the carrier has not been bargaining seriously, and is attempting to blame pilots for its own mismanagement—not least its ‘half-baked’ systemwide preparation for a post-pandemic demand surge in air travel, which Alaska pilots say the company “should have seen coming all along.”

The carrier counters that a new pilot agreement is priority one, but “we must maintain growth and profitability for a strong future.” Claiming to have posted a meager $14m profit in Q4 2021 after $2.3bn in  pandemic period losses, and now reporting a $143m Q1 loss (Wall Street projected $202m), Alaska Air still foresees improvement by June, even plans to boost its fleet by 100 planes to 400 overall, and hire 300 more pilots by year’s end.

pandemic period losses, and now reporting a $143m Q1 loss (Wall Street projected $202m), Alaska Air still foresees improvement by June, even plans to boost its fleet by 100 planes to 400 overall, and hire 300 more pilots by year’s end.

Where they expect to find them amid a pilot shortage lasting as long as seven years surely raises questions of competence and safety at the cockpit controls flying forward, as this isn’t simply a matter of crash courses or OJT. Moreover, more than 375 of the pilots Alaska has hired in recent months are from regional lines with experience solely on small jets or turboprops, while Alaska’s A320 or 737 training capacity is now limited.

Meantime, those contract negotiations are before a federal mediator, which have stalled to impasse thus far. So the carrier is offering a bonus 150% of pay for pilots willing to pickup extra flights—as it was short over 60 pilots in early April—admitting its ‘operational performance’ has been suffering, further impacted by harsh weather across the land. But ALPA warns its Alaska Air pilots are stressed and over stretched as it is, and that over 50 have been already been poached this year by other carriers promising better, easier working conditions.

This, while the airline’s customer service ranks are similarly thinned. Which means suddenly stalled or scrapped flights and up to ten-hour call center wait times, frustrated passengers being grounded, rerouted with last-minute flight-day notification or dished off to competing lines. So we travelers are taking the Alaska squabble and shortage in the shorts, if not contracting bouts of halting ‘terminalitis’, with more airline aggravation and inconvenience baked in by the day. And no amount of splashy “We Care” adverts seem to lighten that load.

Alas, Alaska Air may be the first major carrier stricken by pilot/crew and staffing shortages this spring, but quite likely won’t be the last: A distasteful vernal entrée, to be sure. (MTC…)![]()

EVEN MORE INCREDIBLE SHRINKING MODES.

(5/16/22)—The inevitable post-holiday hangover portends an increase in fretful, untoward layovers well through early 2022.

To be sure, travel demand is down into the new year thus far—what with COVID-Omicron, rough winter weather and the usual January lull. And even leading US airlines are smarting from millions upon millions of dollars in Q4 2021 losses, only Southwest and Alaska Air eking out modest profits.

So rather than soaring forward anew into ’22, most carriers are scaling back. Overall, domestic airline seat  capacity is down some 12% over 2019, internationally off 52%. More specifically, Europe’s capacity is down over 42%—same for Asia, Africa and the Southwest Pacific—South America and the Caribbean upwards of 25%.

capacity is down some 12% over 2019, internationally off 52%. More specifically, Europe’s capacity is down over 42%—same for Asia, Africa and the Southwest Pacific—South America and the Caribbean upwards of 25%.

What these numbers add up to is significant fleet and schedule shrinkage, ‘proactive reductions’ in the parlance of one carrier, an industry wide trimming of seat sales. Take American Airlines (advisedly), which has cut thousands of flights through March, 1-6 runs per daily, out of six cities: New York, Miami, Chicago, Dallas, Phoenix and L.A. The Ft. Worth-based carrier cites, COVID/Omicron infections, winter storms, pilot shortages and fleet delivery delays, but insists it is not actually exiting the cities long term.

Chicago-based United is similarly paring its Q1 schedule, noting steeper labor and fuel costs (jet fuel up 122% of late) as well. Atlanta-based Delta is grounding hundreds of flights in February on, saying it continues to work together around the clock to reroute and substitute aircraft and crews.

JetBlue has cancelled nearly 1,300 flights through January, struggling to get crews back to work sooner, what with COVID cases and staff furloughs. The New York-based carrier is “proactively reducing” flights “with as much notice to customers as possible”—although some of its passengers report phone tree holds of up to five hours.

Even slightly Q4 profitable Southwest Air (Texas) and Seattle-based Alaska Airlines are cutting flight schedules between 10-15%. And these hairy capacity ‘hair cuts’ account for domestic air carriers alone. The only sliver of light on this horizon is the emergence of several scrappy low-fare start-ups, such as Breeze and PLAY Airlines, which seek a competitive edge via exclusively ‘differentiator’ apps and text communication. Alaska-based Northern Pacific, sister of Ravn regional line, plans to launch one-stop service between the US and northeast Asia (on 757s, with an Anchorage stopover) this summer. Meanwhile, Oslo-based Norse Atlantic Airways seeks  a foreign air carrier permit from the Department of Transportation to offer low-cost trans-Atlantic flights between California/Florida and Europe in coming months—routes recently ceded by Norwegian Air.

a foreign air carrier permit from the Department of Transportation to offer low-cost trans-Atlantic flights between California/Florida and Europe in coming months—routes recently ceded by Norwegian Air.

These newbies join Avelo Airlines, a Houston-based ultra low-cost carrier flying to a variety of heretofore ill-served domestic destinations out of Burbank, CA and New Haven, CT with a fleet of 737-700/800 aircraft.

Meantime, the majors’ widespread shrinkage leaves us travelers changing flights, itineraries, departure times, even hubs—if we are able to book a flights (particularly on non-stop routes) and board it at all. Moreover, as airlines adopt this less-is-more operational approach (e.g., easyJet is even stripping away available seat rows), we face the supply/demand conundrum of fewer choices at higher fares owing to arbitrarily limited flights, aircraft and crews.

The air travel squeeze is on, near term anyway. Reason enough why Vamigré will come to the lemon-aid in some potentially sour, if not fitful days ahead. (MTC…)

![]()

A/A to SWA, GOODWILL BLUNTING.

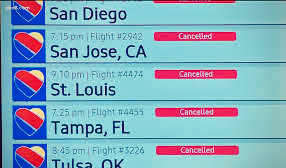

(10/25/21)—Whatever good terms and tidings took flight as pandemic travel restrictions loosened earlier this year were grounded this past holiday weekend as the world’s largest low-cost airline continued stranding thousands of passengers nationwide.

Over those past four days, Southwest Airlines cancelled over 2,300+ flights, delayed hundreds more, with no immediate relief in sight for travelers who have been lining up and camping out at airports coast to  coast, desperately trying and paying dearly to change modes and plans—just like in the bad old pre-COVID days. The spiral of disruptions has cost (aggressively overreaching) SWA $75m in cancellations and exhausted its flight crews and staffs.

coast, desperately trying and paying dearly to change modes and plans—just like in the bad old pre-COVID days. The spiral of disruptions has cost (aggressively overreaching) SWA $75m in cancellations and exhausted its flight crews and staffs.

SWA attributes its latest schedule stripping (nearly 27% of its operational capacity) to foul weather and air traffic control problems plus pandemic-period staffing reductions—not least in Florida (hub to nearly 1/2 of its daily flights)—specifically citing a ‘hiccup’ at the Jacksonville Air Route Traffic Control Center. But the FAA counters that a few hours of military and staff training at the northern Florida facility caused no significant service disruption or air traffic control problems (e.g., affecting less than 2% of carrier operations for American and Spirit).

Instead the federal agency focus is on aircraft and flight crews being situated markedly out of place when the COVID travel slump ended with an unexpected explosion of pent-up summer demand. Southwest  does concede that its fleet and staffing reductions throughout the pandemic via furloughs, buyouts and early retirement packages will make “…getting back to normal more difficult and prolonged,” said SWA Chairman/CEO Gary Kelly. But more schedule paring and capacity crunches may be in order to clear its operational skies, as most all airlines struggle to hire and/or rehire, retrain sufficient pilots and staff.

does concede that its fleet and staffing reductions throughout the pandemic via furloughs, buyouts and early retirement packages will make “…getting back to normal more difficult and prolonged,” said SWA Chairman/CEO Gary Kelly. But more schedule paring and capacity crunches may be in order to clear its operational skies, as most all airlines struggle to hire and/or rehire, retrain sufficient pilots and staff.

Jabs=Jobs?

Still, that doesn’t address the condor in the cockpit here, namely the Dallas-based airline’s recent mandate for companywide COVID vaccinations (or weekly testing) by December 8 (with certain exceptions)—no matter what anti-mandate executive orders come down from the Texas capital. Some headline-grabby politicos are already blaming the industrywide federal VAX directive for SWA’s current system breakdown, suggesting that a pilot walkout may be at work.

The Southwest Airlines Pilots Association (SWAPA) denies any such union stoppage as “false claims”, stating that its members are “…not participating in official or unofficial job actions”, rather ascribing the widespread cancellations/delays to poor company planning—as in overreaching route expansion during the summer travel rebound, scheduling more flights than they can operate. And to date, no other vaccine mandated carriers have so far reported commensurate crew and/or staffing shortfalls—although SWA is surely not the only airline to be facing such logistical meltdowns.

have so far reported commensurate crew and/or staffing shortfalls—although SWA is surely not the only airline to be facing such logistical meltdowns.

In any case, Southwest has already been weathering a quite difficult 2021, with the worst on-time performance and largest percentage of flight cancellations among the four major US airlines in June and July. At the same time its pilots, flight attendants (timing out of FAA allotted air hours) and mechanics—(let alone passengers)—have been complaining about the lofty budget airline’s downdraft and staffing cuts (some 7,000 fewer employees than in pre-pandemic times). Some assert that Southwest routing/operations have become “brittle and subject to massive failures under the slightest pressure”, what with out-of-position aircraft and tightly margined crews scattered, stranded to the winds.

An unsparing assessment to be sure, but given how bluntly the carrier is throttling the goodwill of its travel-hungry passengers, not exactly out of place thus far—absent some quick SWA qualitative pleasing and quantitative easing.

(10/31/21)—Southwest is not flying solo on this count, however, as the Utah-Based SkyWest regional airline had to cancel (463) and delay (900) more flights October 21-22 due to cascading “operational disfunction: i.e., its crews and aircraft were “out of position.” Now, et tu, American Airlines—cancelling nearly 2k flights over the Halloween weekend (12% of its operations), delaying nearly 30% of its entire capacity—citing, what else: foul weather (limited to 2 of 5 runways in windy DFW) and staffing shortages (of flight attendants and ground crews). Trick or mistreat?(MTC…)